Cybercriminals on underground forums and in private chat groups are increasingly developing structured fraud schemes designed to exploit weaknesses in financial institutions’ operational processes. Rather than relying on isolated or opportunistic scams, these discussions reveal an organized, process-driven approach that combines stolen identity data, social engineering, and a deep understanding of financial workflows.

In these discussions, smaller financial institutions—particularly small and mid-sized credit unions—are frequently identified as attractive targets due to perceived gaps in identity verification procedures and limited fraud prevention resources.

Researchers recently uncovered a detailed loan fraud method circulating within one such underground group. The scheme outlines how fraudsters can pass credit history checks, identity verification, and loan approval processes by using stolen identities while avoiding traditional security controls.

Rather than exploiting software vulnerabilities, the approach focuses on manipulating legitimate onboarding and lending workflows, making fraudulent applicants appear to be genuine customers throughout the process.

The published methodology follows a systematic, step-by-step structure, breaking the scheme down from identity theft to loan approval in a way that can be consistently replicated, highlighting the increasingly organized nature of modern fraud operations.

Знімок екрана методу, поширеного в групі чату, що показує відкриття зловмисника

An Identity-Driven Process Rather Than a System Intrusion

At its core, this approach relies on obtaining enough personal information to convincingly impersonate a legitimate borrower. This includes identifiers such as names, addresses, dates of birth, and, in some cases, information related to the victim’s credit history.

A typical example of an underground identity fraud guide.

The entire process is digital, with the attacker using a stolen identity to submit a loan application. This distinction is critical: the attack does not “hack” the system but instead exploits weaknesses in how it is designed and operated.

A key component of the method is the ability to pass identity verification, particularly checks based on Knowledge-Based Authentication (KBA). These systems typically rely on questions related to:

Previous addresses

Loan or credit history

Employment or family associations

In practice, much of this information can be reconstructed or inferred from publicly available records, social media profiles, previously leaked datasets, and aggregated identity databases.

The method demonstrates how fraudsters can anticipate these verification checks and prepare for them in advance, effectively turning identity verification into a predictable step rather than a meaningful barrier.

It also illustrates how controls once considered reliable for identity verification can be studied, adapted, and ultimately exploited by cybercriminals who develop identity theft techniques specifically to collect the information needed to bypass these requirements.

By the time a fraudulent loan application reaches a financial institution, most of the work has already been completed. Criminals have already obtained stolen personal information, KBA answers, and the victim’s financial history from dark web forums and underground marketplaces—long before they ever interact with the institution.

Fraud Workflow: Step by Step

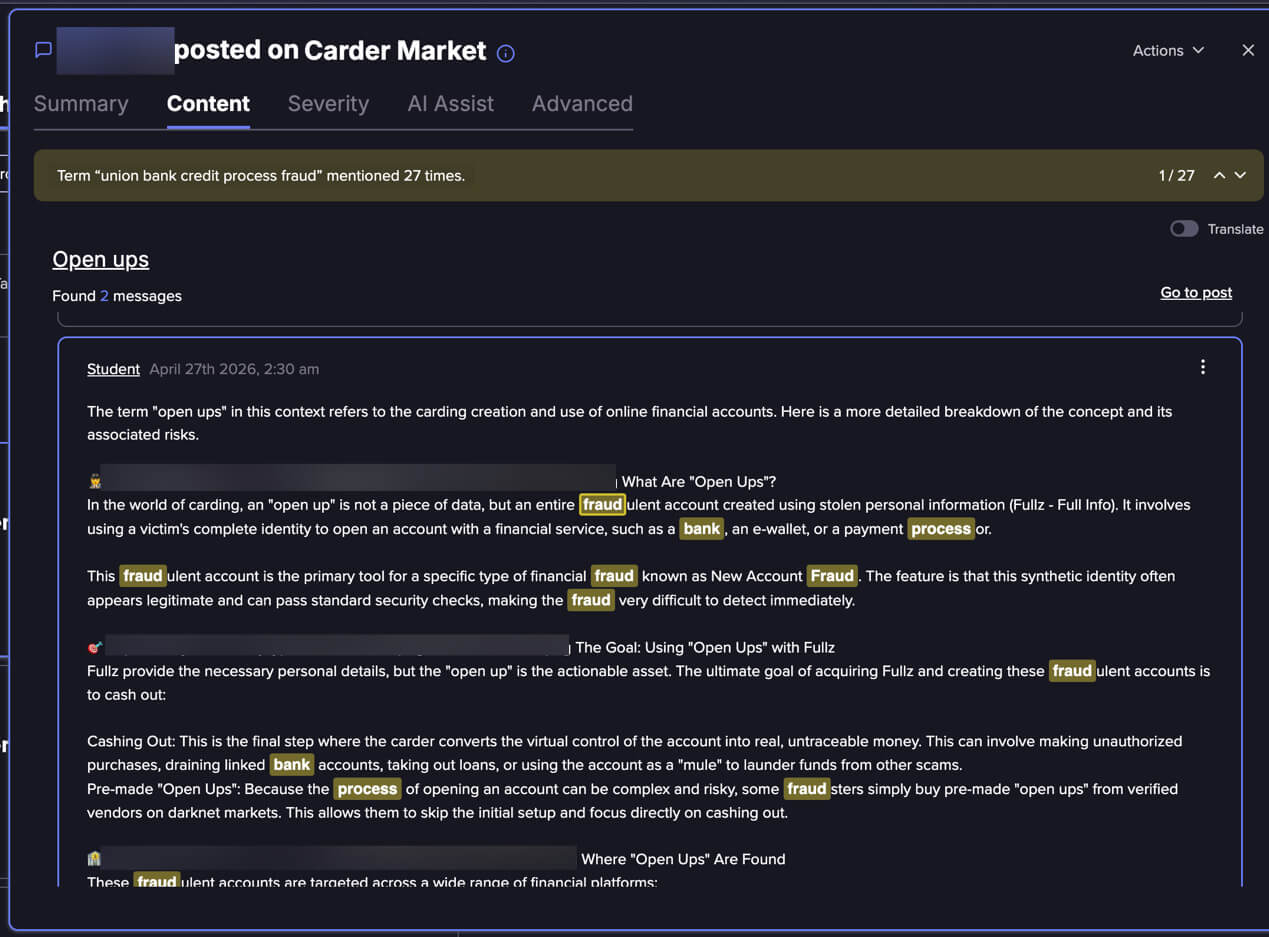

Obtaining identity data: Stolen personal information is acquired, including complete identity details and background information sufficient to impersonate a legitimate individual.

Assessing the credit profile: The attacker reviews the victim’s financial profile to determine loan eligibility and the likelihood of approval.

Preparing for verification (KBA readiness): Additional personal information is collected to anticipate and correctly answer identity verification questions.

Selecting the target: Small and mid-sized credit unions are chosen based on their perceived weaker verification procedures and less mature fraud detection capabilities.

Submitting the loan application: A loan application is filed using the stolen identity, ensuring that all submitted information is consistent and credible.

Passing identity verification: Knowledge-Based Authentication (KBA) and standard identity checks are successfully completed, reinforcing the appearance of legitimacy.

Loan approval and fund disbursement: The financial institution approves the loan and releases the funds through its normal lending process.

Moving and cashing out the funds: The money is transferred to controlled accounts, routed through intermediary accounts, and ultimately withdrawn or converted to complete the monetization process.

Why Small and Mid-Sized Credit Unions Are Targeted

One of the most notable aspects of this method is its focus on smaller financial institutions. Rather than targeting large banks or highly secured fintech platforms, fraudsters appear to favor small and mid-sized credit unions, which they perceive as being more likely to:

Rely on traditional identity verification methods;

Have less advanced behavioral fraud detection capabilities;

Prioritize customer accessibility over stricter security controls.

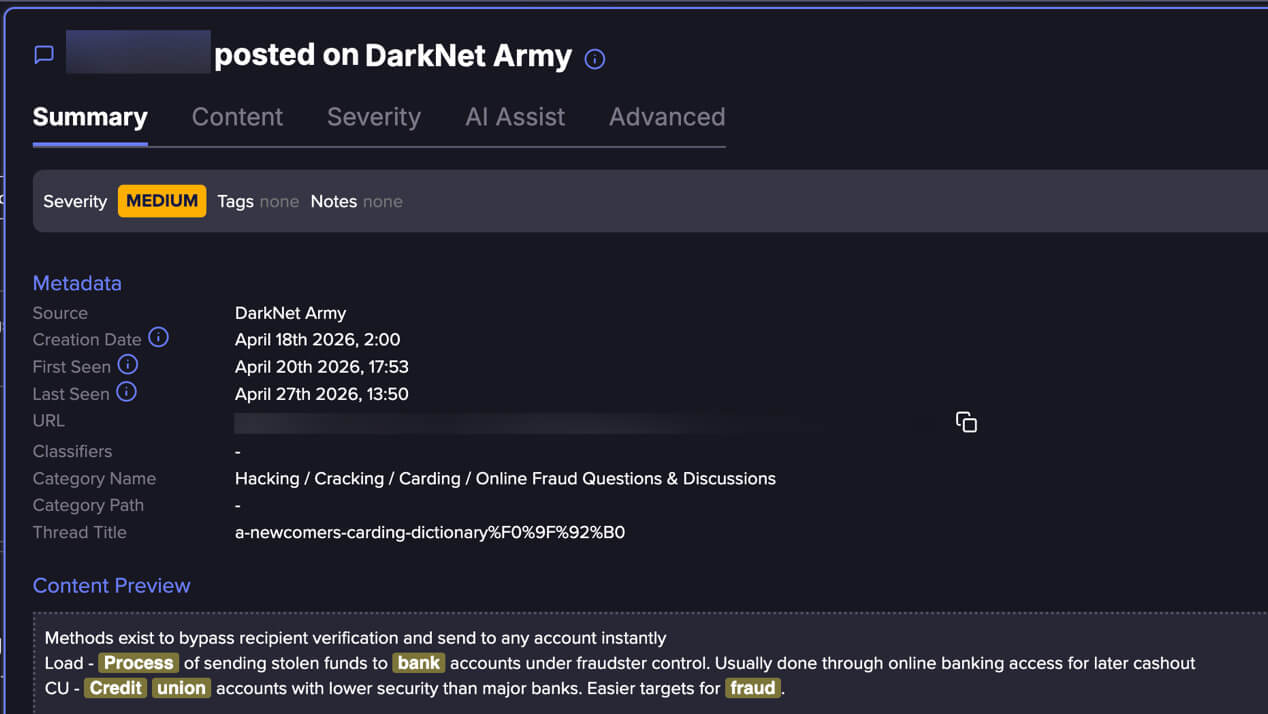

The attacker explains that CU accounts have lower levels of security than those at major banks and are therefore easier targets for fraud.

Although this perception is not universally accurate, it is enough to influence attackers’ behavior, directing them toward institutions they believe offer a higher chance of success.

Recent industry reports support this trend. Fraud losses in the auto lending sector alone are projected to reach $9.2 billion in 2025, with smaller and regional lenders expected to face increasing pressure from organized fraud operations.

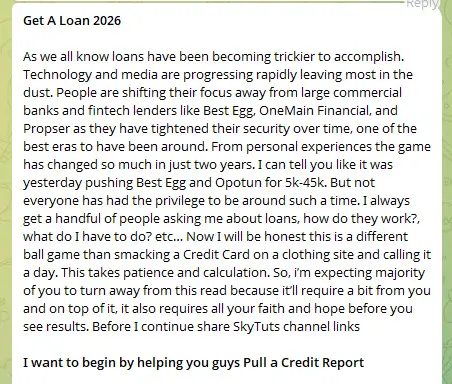

The attacker discusses methods for obtaining loans.

Cash-Out and Monetization

Once a loan is approved, the operation enters its most critical phase—turning access into money. By this stage, the attacker has already completed the most difficult part of the scheme: passing identity verification and establishing trust under a stolen identity. From the institution’s perspective, the transaction appears legitimate, and the funds are disbursed through the same standard channels used for genuine customers.

The focus then shifts to speed and separation. Rather than leaving the funds in the original account, the money is quickly transferred, often through intermediary accounts, creating distance from its source.

This stage overlaps with broader fraud ecosystems, where access to additional accounts and financial channels enables attackers to route, split, or redistribute funds, making them more difficult to trace.

The cash-out phase is particularly effective—and difficult to detect—because each individual transaction resembles normal financial activity. Transfers, withdrawals, and account movements are not inherently suspicious on their own.

Instead, the risk lies in how these actions are linked together over a short period of time, allowing attackers to complete the cash-out process before automated detection systems or manual reviews can intervene.

Who Is Most at Risk?

This method provides insight into the individuals and institutions most likely to be targeted for identity theft.

People with established credit histories – Attackers benefit from targeting individuals with strong or stable credit records, increasing the likelihood that loan applications will be approved.

People with a significant online presence – Individuals who share large amounts of personal information online may unintentionally expose details that can help fraudsters pass identity verification checks.

Customers of smaller financial institutions – Clients of small and mid-sized credit unions may face greater risk if their institutions rely on less advanced fraud detection systems.

This loan fraud method demonstrates how financial crime is evolving. Rather than attacking systems directly, cybercriminals are increasingly targeting the business processes that surround them, exploiting identity, predictability, and trust to achieve their objectives.

As these techniques become more structured and widely shared, the line between legitimate activity and fraud continues to blur, making detection more difficult and increasing the need for more adaptive fraud prevention strategies.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.